Costing

Costing is same as cost accounting as it also includes the cost incurred in the production. Costing includes fixed, variable and manufacturing cost of the product. Costing is also known as absorption costing.

Setting Standard Costs – Ideal and Practical Standards: Learning Objective of the Article: Who provide the inputs in setting standard costs? Define and explain ideal and practical standards. What is the difference between budgets and standards? What is the purpose of standard costing? Setting

Definition: Reciprocal method is a method of allocating service department costs to other departments that gives full recognition to interdepartmental services. Explanation: The reciprocal method gives full recognition to interdepartmental services. Under the step method, only partial recognition of interdepartmental services is possible. The

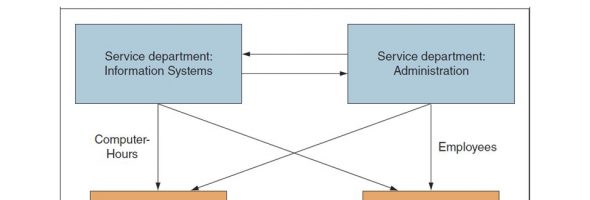

Service Department Costing: After studying this chapter you should be able to: Difference between service department and operating department: Most of the large organizations have both operating departments and service departments. The central purpose of the organization are carried out in the operating department.

Selecting Allocation Base: Costs are ordinarily assigned to products and services by using a two stage process. In first stage, service department and other costs are allocated to operating departments. In second stage, the costs that have been assigned to operating departments are allocated

Learning Objective of the Article: Define and explain target costing. Compute the target cost for a new product or service. What are advantages and disadvantages of target costing approach. In traditional costing system it is presumed that a product has already been developed, has

Overall or Net Factory Overhead Variance: Definition: Overall or net factory overhead variance is the difference between actually incurred factory overhead and expenses charged into process using the standard factory overhead rate. Formula of Overall or Net Factory Overhead Variance: Overall or net overhead

Normal Costing System Definition: Normal Costing system is a costing system in which overhead costs are applied to jobs by multiplying a predetermined overhead rate by the actual amount of the allocation base incurred by the job.

Definition and Explanation of Operating Leverage: A lever is a tool for multiplying force. Using a lever, a massive object can be moved with only a modest amount of force. In Business, operating leverage serves a similar purpose. Operating leverage is a measure of

Direct Materials Price and Quantity Standards: Learning Objective of the articles: Define and explain direct materials price standards and direct materials quantity standards. Explain how direct materials price and quantity standards are set? Contents: Direct Materials Price Standards Direct Materials Quantity Standards Example of

Direct Materials Quantity Variance: Learning Objective of the articles: Define and explain “direct materials quantity variance” and its significance. How is it calculated? How direct materials quantity variance is interpreted? What are the reasons / causes of a favorable and unfavorable direct materials quantity

Direct Materials Price Variance: Learning Objective of the articles: Define and explain “direct materials price variance” and its significance. How is it calculated? How direct materials price variance is interpreted? What are the reasons / causes of unfavorable or favorable materials price variance? Contents:

Direct Labor Standards: Learning Objective of the articles: Define and explain “direct labor standards” . How direct labor rate and direct labor efficiency standards are set? Direct labor price and quantity standards are usually expressed in terms of a labor rate and labor hours.

Limitations of Cost-Volume-Profit (CVP) Analysis: Cost volume profit (CVP) is a short run, marginal analysis: it assumes that unit variable costs and unit revenues are constant, which is appropriate for small deviations from current production and sales, and assumes a neat division between fixed

Direct Labor Rate | Price Variance: Learning Objective of the articles: Define and explain “direct labor rate | price variance /labour rate variance” . How direct labor rate or price variance rate is calculated? What are the reasons / causes of favorable and unfavorable

Direct Labor Efficiency Variance Learning Objective of the article: Define and explain “direct labor efficiency | usage variance” . How direct labor efficiency (labour analysis) or usage variance is calculated? What are the reasons / causes of unfavorable or favorable labor efficiency variance? Contents:

Margin of Safety (MOS): Learning Objectives: Define and explain margin of safety. Calculate margin of safety ratio. What is its significance/importance? Contents: Definition of Margin of Safety (MOS) Formula of MOS Example Review Problem Definition and Explanation: Margin of safety (MOS) is the excess

Difference Between Gross Margin and Contribution Margin: Learning Objectives: What is the difference between gross margin and contribution margin? Gross Margin is the Gross Profit as a percentage of Net Sales. The calculation of the Gross Profit is: Sales minus Cost of Goods Sold. The

Assumptions of Cost-Volume-Profit (CVP) Analysis: Learning Objectives: What are underlying assumptions of cost volume profit (CVP) analysis? A number of assumptions underlie cost-volume-profit (CVP) analysis: These cost volume profit analysis assumptions are as follows: Selling price is constant. The price of a product or