Cost Volume Profit (CVP) Relationship in Graphic Form

Cost Volume Profit (CVP) Relationship in Graphic Form:

Learning Objectives:

- Prepare a CVP graph or breakeven chart.

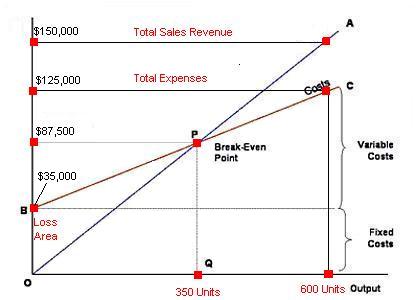

The relationships among revenue, cost, profit and volume can be expressed graphically by preparing a cost-volume-profit (CVP) graph or break even chart. A CVP graph highlights CVP relationships over wide ranges of activity and can give managers a perspective that can be obtained in no other way.

Preparing a CVP Graph or Break-Even Chart:

In a CVP graph some times called a break even chart unit volume is commonly represented on the horizontal (X) axis and dollars on the vertical (Y) axis. Preparing a CVP graph involves three steps.

1. Draw a line parallel to the volume axis to present total fixed expenses. For example we assume total fixed expenses $35,000.

|

|

2. Choose some volume of sales and plot the point representing total expenses (fixed and variable) at the activity level you have selected. For example we select a level of 600 units. Total expenses at that activity level is as follows:

| Fixed Expenses | $35,000 |

| Variable Expenses (150×600) | $90,000 |

| ——— | |

| Total Expenses | $125,000 |

| ====== |

After the point has been plotted, draw a line through it back to the point where the fixed expenses line intersects the dollars axis.

3. Again choose some volume of sales and plot the point representing total sales dollars at the activity level you have selected. For example we have chosen a volume of 600 units. sales at this activity level are $150,000 (600units × $250) draw a line through this point back to the origin. The break even point is where the total revenue and total expense lines cross. See the graph and note that break even point is at 350 units. It means when the company sells 350 units the profit is zero. When the sales are below the break even the company suffers a loss. When sales are above the break even point, the company earns a profit and the size of the profit increases as sales increase.

You may also be interested in other articles from “cost volume profit relationship” chapter

- Contribution Margin and Basics of CVP Analysis

- Difference Between Gross Margin and Contribution Margin

- Cost Volume Profit (CVP) Relationship in Graphic Form

- Contribution Margin Ratio (CM Ratio)

- Importance of Contribution Margin

- Change in fixed cost and sales volume

- Change in variable cost and sales volume

- Change in fixed cost, sales price and sales volume

- Change in variable cost, fixed cost, and sales volume

- Change in regular sales price

- Break even point analysis (calculation of break-even point by contribution margin and equation method)

- Target profit analysis

- Margin of safety

- Sales Mix and Break Even with Multiple Products

- Cost Volume Profit (CVP) Consideration in Choosing a Cost Structure

- Operating Leverage and degree of operating leverage

- Assumptions of Cost Volume Profit (CVP) Analysis

- Limitations of Cost Volume Profit Analysis

Other Related Accounting Articles:

- Effect of Change in Variable Cost and Sales Volume on Contribution Margin and Profitability

- Limitations of Cost-Volume-Profit (CVP) Analysis

- Effect of Change in Variable Cost, Fixed Cost and Sales Volume on Contribution Margin and Profitability

- Cost Volume Profit Relationship – (CVP Analysis)

- Effect of Change in Regular Sales Price on Contribution Margin and Profitability

- Importance of Contribution Margin – Advantages of Cost Volume Profit (CVP) Analysis

- Assumptions of Cost-Volume-Profit (CVP) Analysis

- Effect of Change in Fixed Cost and Sales Volume on Contribution Margin and Profitability

- Cost Volume Profit (CVP) Formulas

- Contribution Margin and Basics of Cost Volume Profit (CVP) Analysis

Or

Download E accounting book in MS-word format for just 20 $ - Click here to Download