Financial Statement Analysis

Financial statement analysis is the analysis or reviewing the balance sheet, profit and loss account which helps in better decision making by company. If the financial statement analysis is good, strong by the people it is useful for company along with investors, managers and others. Financial statement analysis is also helpful in determining the performance of company in over pas years.

Current Assets to Proprietor’s Fund Ratio: Current Assets to Proprietors’ Fund Ratio establishes the relationship between current assets and shareholder’s funds. The purpose of this ratio is to calculate the percentage of shareholders funds invested in current assets. Formula: Current Assets to Proprietors Funds

Creditors / Accounts Payable Turnover Ratio: Definition and Explanation: Credit turnover ratio is similar to the debtors turnover ratio. It compares creditors with the total credit purchases. It signifies the credit period enjoyed by the firm in paying creditors. Accounts payable include both sundry creditors

Definition and Explanation of Horizontal or Trend Analysis: Comparison of two or more year’s financial data is known as horizontal analysis or trend analysis. Horizontal analysis is facilitated by showing changes between years in both dollar and percentage form as has been done in the example below. Showing changes in dollar

Financial Statement Analysis Learning Objectives: Prepare and interpret financial statements in comparative and common-size form. Compute and interpret financial ratios that would be most useful to a common stock holder. Compute and interpret financial ratios that would be most useful to a short-term creditor

Generally Accepted Accounting Principles (GAAP): Generally accepted accounting principles (GAAP) are those principles that have substantial authoritative support. The AICPA’s code of professional conduct requires that members prepare financial statements in accordance with generally accepted accounting principles (GAAP). Specifically rule 203 of this code

Fixed Assets Turnover Ratio: Definition: Fixed assets turnover ratio is also known as sales to fixed assets ratio. This ratio measures the efficiency and profit earning capacity of the concern. Higher the ratio, greater is the intensive utilization of fixed assets. Lower ratio means

Fixed Assets to Proprietor’s Fund Ratio: Definition: Fixed assets to proprietor’s fund ratio establishes the relationship between fixed assets and shareholders funds. The purpose of this ratio is to indicate the percentage of the owner’s funds invested in fixed assets. Formula: Fixed Assets to

Accounting Ratios | Financial Ratios: Learning Objectives: Define and explain the term accounting ratios. What are advantages and limitations of using accounting or financial ratios. How financial ratios are classified. Ratios simply means one number expressed in terms of another. A ratio is a

Financial Accounting Ratios and Formulas: This is a collection of financial ratio formulas which can help you calculate financial ratios in a given problem. Analysis of Profitability: General profitability: Gross profit ratio = (Gross profit / Net sales) × 100 Operating ratio = (Operating

In this article we will discuss how to calculate expense ratio in insurance and total expense ratios meaning with calculation with ratio formula Definition: Expense ratios indicate the relationship of various expenses to net sales.The operating ratio reveals the average total variations in expenses.

Proprietary Ratio or Equity Ratio: Definition: This is a variant of the debt-to-equity ratio. It is also known as equity ratio or net worth to total assets ratio. This ratio relates the shareholder’s funds to total assets. Proprietary / Equity ratio indicates the long-term

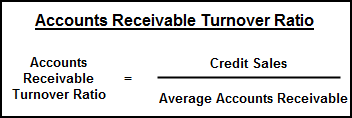

Debtors Turnover Ratio | Accounts Receivable Turnover Ratio: A concern may sell goods on cash as well as on credit. Credit is one of the important elements of sales promotion. The volume of sales can be increased by following a liberal credit policy. The